Sustainable Investors Might Soon Get the Clarity they Need, if the SEC’s New Proposal Can Survive Legal Challenges

A protest against banks' investment into fossil fuels (Photo by Visible Hand)

Over the past few years, a “tectonic shift” to sustainable investing has defined the financial sector. Environmental, Social, and Governance (ESG) metrics, such as carbon emissions, that evaluate company performance based on factors outside of traditional financial accounts are at the core of what it means to invest sustainably in the 21st century. Today, 92% of companies listed on the S&P 500 publish a sustainability report and investors are rushing to integrate ESG considerations into their portfolios, driving the 12-fold increase of money that flowed into sustainable funds from 2016 to 2020. But a lack of reporting standards in the U.S. has let some companies and investors mischaracterize their assets as “green” and caused havoc for investors trying to make decisions using inconsistent and incomparable information.

In March 2022, following in the footsteps of the EU—which already requires robust corporate sustainability reporting—the U.S. Securities and Exchange Commission (SEC) issued a proposal designed to usher the U.S. public sector into a new era of climate-oriented disclosures. The proposed rule, expected to come into effect early next year, would require public companies to report climate-related information, such as carbon emissions and material climate-related risks, in their annual financial statements. Though many in the business, political, and nonprofit sectors have voiced support for the proposal, it is far from perfect and will require heavy revision ahead of implementation if it is to survive imminent litigation and succeed in its mission to provide consistent climate-risk information to the market. The proposal is a key part of the Biden Administration’s plan to achieve net zero emissions by 2050, and has been praised by investors, companies, NGOs, and academics for formalizing and centralizing the “E” in ESG reporting standards. In the face of a Republican-controlled Congress in the House, executive regulation like this proposal, rather than congressional legislation, will be a key factor to achieving the Biden Administration's climate goals.

However, in light of the Supreme Court’s recent ruling that the EPA exceeded its power by regulating carbon emissions, the SEC is concerned that the rule might be struck down by the judiciary. Opponents of the proposal in the corporate world and the Republican party have already threatened litigation, and the U.S. Chamber of Commerce, a powerful trade group, wrote that the proposed rules “are vast and unprecedented in their scope, complexity, rigidity and prescriptive particularity.” Others disagree with the entire principle of the government regulation of ESG metrics, arguing that the complexity of ESG means that a one-size-fits-all model will not work on considerations that inherently vary from company to company.

One of the most substantial objections to the proposal center on the definition of materiality and the legal purview of the SEC, whose regulatory mandate to maintain fair and efficient markets hinges on the requirement that businesses disclose material information. Materiality is a legal concept that serves to determine what information companies are required to make to the public so that they can make an risk-informed investment decision. Drawing from relevant case law, the SEC states its definition of materiality to be information for “which there is a substantial likelihood that a reasonable investor would attach importance.” This definition is maintained in the language of the proposal, which points to the impact of California wildfires on farmers and wineries as an example of a material climate-related impact. However, the interpretations of who the “reasonable investor” is and what it is they care about are still up for debate among legal scholars.

A current commissioner dissented from the proposal, saying that the disclosure requirements were made “without regard for materiality.” Five former commissioners concurred, writing in a dissenting comment that the SEC would be exceeding their legal authority by mandating politically-charged disclosures that are an “unprecedented and unjustified effort beyond financial materiality.” Their arguments imply that a company’s impact on the environment—its carbon emissions—has no bearing on a company’s financial performance and, therefore, are not important to the “reasonable investor” seeking a financial profit. Another group of former commissioners, however, argue that the SEC has used its “authority to require environmental and climate-related disclosures” for decades, and therefore is well within their legal right to propose the new mandates.

Voicing another potential reason why the SEC’s proposal could be in violation of materiality constraints, J.W. Verret, a professor at the Antonin Scalia Associate Law School, suggests that the disclosures are not based on the “reasonable investor,” but rather to appease powerful, vocal, and special-interest investors such as pension and union funds. Thus, he claims, the SEC has exceeded its legal purview because the proposed disclosures are immaterial.

Yet the question as to who counts as a “reasonable investor” is still contentious. A group of law professors commented that disclosure requirements must evolve with a changing market. In a press release, SEC Chairman Gary Gensler illustrated how the market landscape, and thus the “reasonable investor,” have changed with the growing understanding of impending environmental impacts. Gensler said that because investors who represent “literally tens of trillions of dollars” are “recogniz[ing] that climate risks can pose significant financial risks to companies,” they have a burgeoning need for climate disclosures. Furthermore, it could be argued that the “reasonable investor” is beginning to care more about the environmental and social impacts of their investments beyond financial implications. A recent study by Stanford Business School found that younger investors claim they are willing to sacrifice 6-10% of their retirement savings to “support ESG causes,” hinting at a potential shift in the mindset of the new reasonable investor that broadens the concept of company performance beyond financial profit.

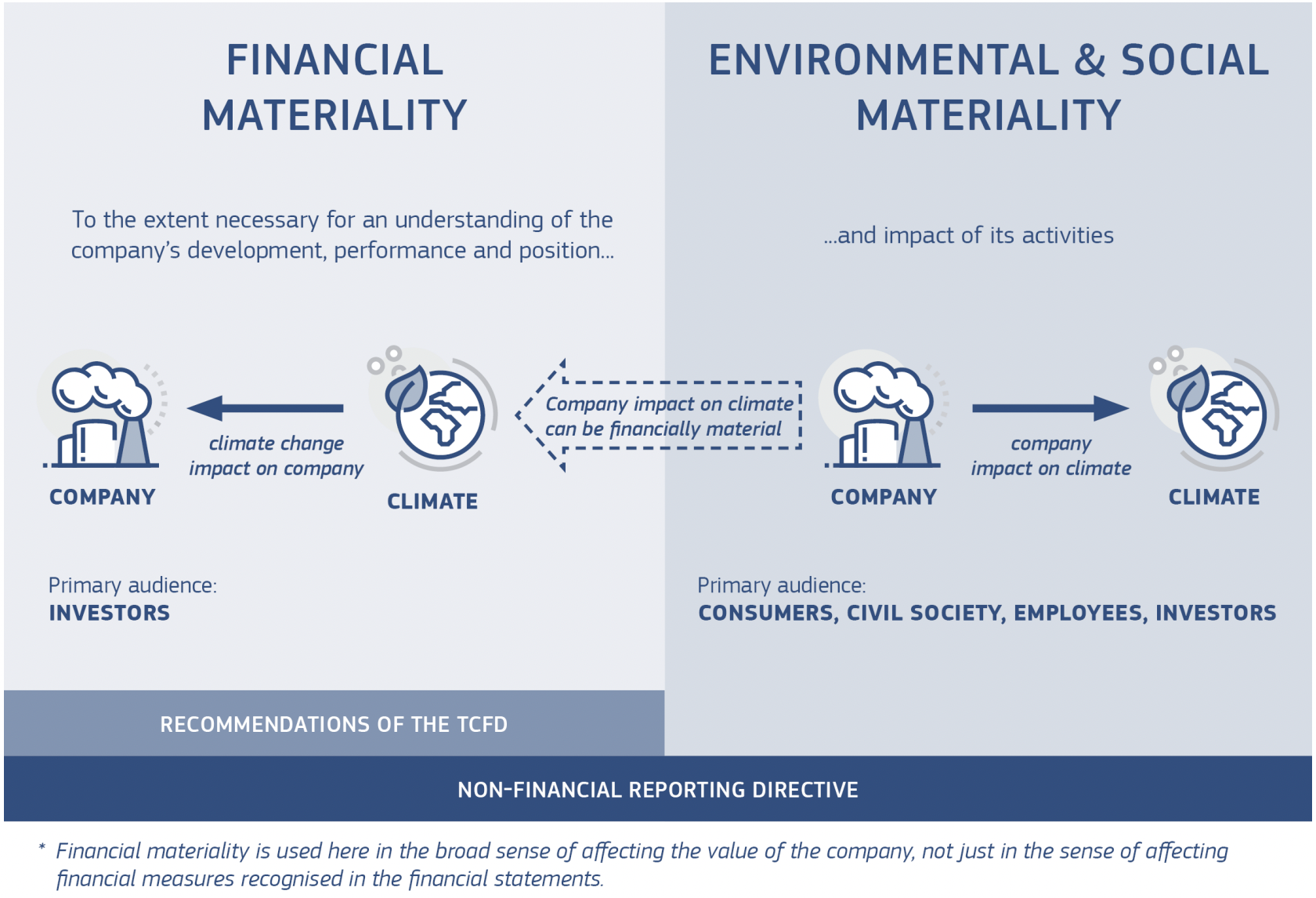

Going even further to expand materiality to include a non-financial dimension, the EU introduced a new concept called double materiality, which looks at materiality from two perspectives: 1) financial and 2) environmental and social. While the internally-facing financial component is what materiality traditionally considers to be important information, double materiality adds another viewpoint that includes a company’s “external impacts” in its appraisal of company value.

Within this conception of double materiality, London School of Economics PhD student Mattias Täger identified a divide between what he terms “weak” and “strong” double materiality with regard to climate information. With the weak interpretation, non-financial information, such as compliance with strengthening regulation or ability to attract talent, is considered important because of its direct impact to a firm’s bottom line. This weak interpretation finds the environmental and social materiality components to be material because they pose financial risk to the firm’s performance. With the strong interpretation, however, the environmental and social components are considered important by the “reasonable investor” for reasons beyond purely financial performance.

It is unclear whether the SEC will follow the EU’s lead and adopt this new definition of materiality, let alone if it is legal to do so. Current SEC commissioner Hester Pierce—the only commissioner to disapprove of the proposal—argued that double materiality “has no analogue in our regulatory scheme.” Once the proposal is in its revised form, it will surely face litigation that will determine the future of materiality in U.S. law, and the extent to which the financial sector can participate in the global fight against climate change.

Carmen Vintro is a Senior Editor for CPR and a senior at Barnard studying English with minors in philosophy and economics. When she’s not submerged in a Keats or Whitman poem, or conversing with friends about how we are living in the Heideggerian technological age, Carmen loves thinking a little more practically about where the world is heading.

This article was submitted to CPR as a pitch. To write a response, or to submit a pitch of your own, we invite you to use the pitch form on our website.